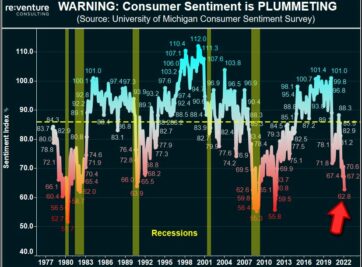

90% Chance: RECESSION in 2022?

Oil Prices are Surging. Consumer Sentiment is Crashing. The odds of a 2022 Recession have SKYROCKETED in recent months.

We’re now firmly entrenched in 2021. People are doing their best to look forward and forget the trials and tribulations of the previous year. But for real estate investors there is no such luxury. Understanding the recent trends in growth and appreciation is paramount for staying ahead of the curve and maintaining a sound investment strategy.

Despite the recession and pandemic, real estate values in 2020 went through the roof. The average market grew values at +8.4% in 2020, but with significant variation surrounding that average. In this post we will break down the Best and Worst performing real estate markets of 2020 and provide insight into what to expect for them going forward.

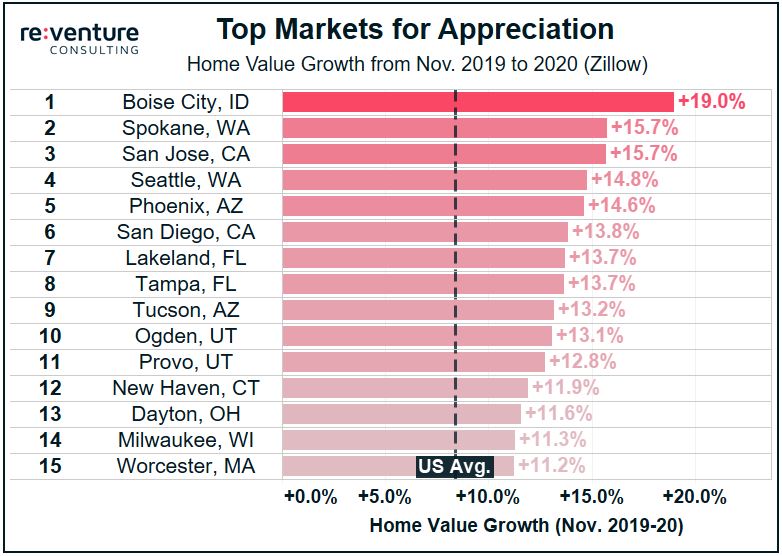

Let’s start off with the fun stuff: the Best Markets. Those with the most appreciation in 2020 according to Zillow. Investors in these markets experienced value appreciation of over 10% in the previous year – some even approaching 20%. But the million dollar question surrounding these markets is: Will the growth last?

Prudent investors should be cautious entering any of the above markets right now. Seeing growth rates like +15% is a warning flag. Regardless of the underlying fundamentals, those levels of appreciation are impossible to sustain. If you do want to chase growth, do it in the markets that are affordable and permitting fewer new housing units (Spokane, Tucson, Milwaukee). Their fundamentals are on firmer footing.

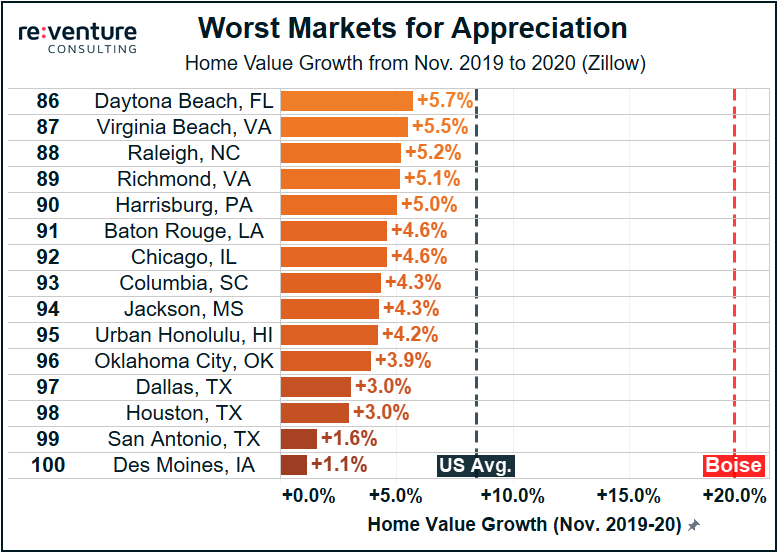

Now to turn our attention to the dogs. The markets that struggled to take part in the housing market boom of 2020. Most of these markets came in at appreciation rates of 3-5%, solid for normal times but ultimately lacking when other markets were putting up 15%+.

Just because a market had low real estate appreciation in 2020 doesn’t mean it’s a bad market to invest in. It could just mean the market is “slow and steady”. This more manageable rate of growth will likely make these markets more durable during a downturn, and more likely to achieve growth coming out of a downturn. Maybe Slow and Steady wins the race?

Reventure Consulting provides predictive analytics to real estate owners, developers, and lenders looking for the locations to invest their capital. Reach out today to learn more about how Reventure can help you achieve better returns.

Oil Prices are Surging. Consumer Sentiment is Crashing. The odds of a 2022 Recession have SKYROCKETED in recent months.

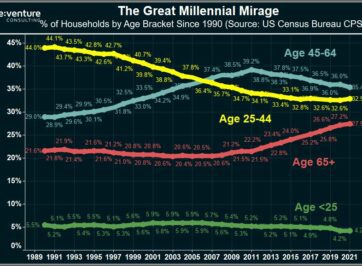

Millennials are supercharging the 2022 Housing Market, right? Wrong according to data from the US Census. In fact, Millennials are BOYCOTTING the Market.

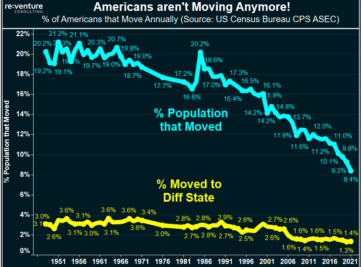

Home Prices are up 20-30% across states like Florida and Texas in 2021. But there’s no growth in the number of people moving there. Is this a colossal bubble?

How bad will the 2021 Housing Crash be? Find out by looking back in history at the WORST Housing Crashes of all-time.

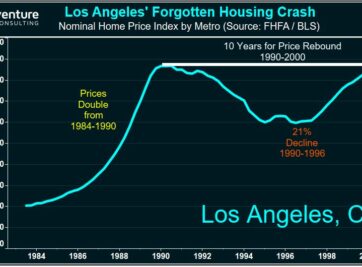

Florida’s Housing Market is BOOMING in 2021. But could the state be heading for another 50% crash in Home Prices? Certain data says that’s a possibility.

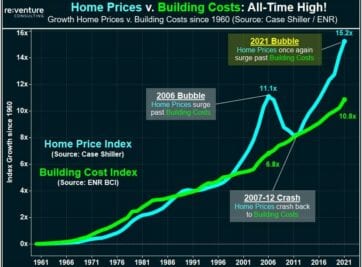

Surging Construction Costs in 2021 are being blamed for the Housing Market Mania being experienced in the US. Yet the data tells a very different story.

Where are the real estate markets that offer home buyers and investors the most value during the 2021 Housing Bubble? Reventure Consulting teaches you how to use data to find them!

Many pundits try to argue that the US is facing a housing shortage crisis. These people are wrong. In fact, the demographic data says the exact opposite – that there is a shortage in DEMAND for homes.

Prices in the US Housing Market are at record levels in 2021 relative to wages and inflation. Yet we’re in a deep economic recession. How could this be? Well, blame HGTV.

Sign up to hear insights from Reventure