There’s a number of false narratives that the mainstream real estate media, along with realtors, perpetrate about the US Housing Market. Perhaps the worst, and most false, is regarding Millennials.

The narrative goes like this: the number of Millennials (think those aged 25 – 44) in America is higher than it has ever been before. These Millennials are at peak home-buying age and provide today’s Housing Market with voracious demand. And this demand will continue into the foreseeable future, providing support for continued home price growth.

Unfortunately for the US Housing Market heading into 2022, the reality is exactly the opposite. Millennials, rather than supporting the market today, are a big DRAG on the Housing Market.

Don’t believe me? Consider the following:

The Millennial (aged 25-44) share of Housing Demand in America has plummeted over the last 30 years.

Millennials are not able to afford the sky-high down payments in today’s Housing Market.

Millennials are delaying life events like marriage and having children, or forgoing them altogether.

Millennials are boycotting the US Housing Market (although not necessarily by choice). This Millennial Boycott will ultimately hasten the Housing Crash rather than continue to sustain prices and growth. Let’s dig into the data!

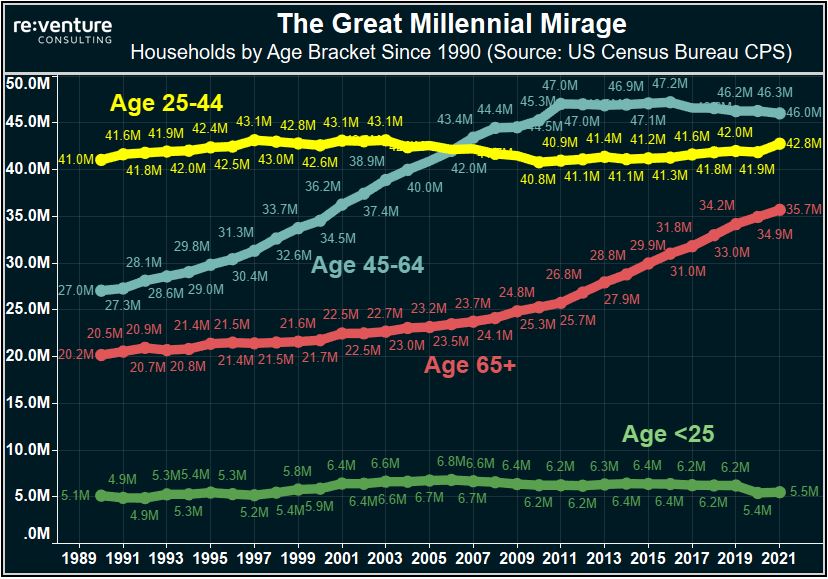

Fewer Millennials Demanding Real Estate

There’s roughly 72 Million Millennials in America today, born between 1981 and 1996 and aged 25 to 40 years old. They are currently the largest generational segment, now bigger than Baby Boomers and Gen X. This stylized fact leads many down the incorrect road of thinking that Millennials are a big driver of Housing Demand in 2021/2022.

But looking into data historically shows that the share of housing demand coming from that key home-buying age segment has declined significantly.

Consider this: the number of aged 25-44 year old households (the age segment roughly corresponding with today’s Millennials) occupying homes and apartments has stagnated over the last 30 years!

No Growth in Housing Demand from the 25-44 age segment over the last 30 years. (Source: US Census Bureau)

Munch on that for a second…the number of 25-44s occupying a home or apartment has stayed in a range of 41-43 Million, experiencing NO GROWTH over the last three decades. Same goes for the under 25 segment.

Rather than from Millennials, recent growth in Housing Demand comes squarely from one demographic: Seniors (65+)! They’ve increased their Household Count from a scant 20 Million in 1990 all the way up to 36 Million in 2021 (74% growth).

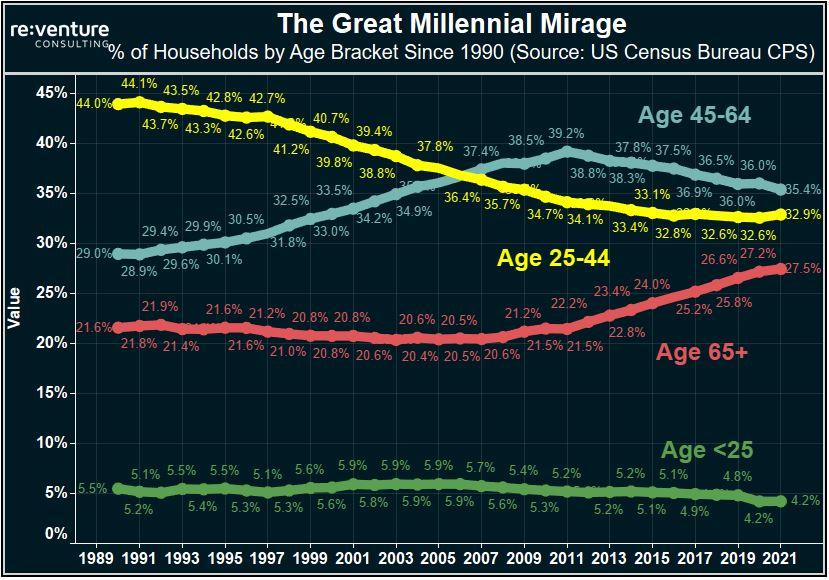

But get ready for this next graph. Things look even starker when we evaluate the share of US Housing Demand by age segment, rather than just raw figures.

Huge Declines in the % of Homes/Apartments occupied by the Millennial age segment. (Source: US Census Bureau)

The key 25-44 segment occupied 44% of Homes and Apartments back in 1990 – by far the most predominant demographic age group back then. But fast forward to 2021 and that share has slipped to 33%, and is now second to the 45-64. The only age segment which is capturing a growing share of Housing Demand over the last decade is once again, Seniors (65+)! They’ve shot up from 21% in 2010 to nearly 28% in 2021.

Remember this: Seniors are leading real estate demand in America in 2021. And they will continue to do so over the next decade. Millennials are in the backseat, both in raw numbers and perhaps more importantly, finances.

Millennials Can’t Afford It in 2021

Home prices, along with the down payments needed to buy a home, have skyrocketed over the last 30 years. For instance, in 1989 the typical home only required a $5,000 down payment at 5% down ($100k price)!

But not anymore. Fast forward to late 2021/early 2022 and the typical down payment has more than tripled to $16,000. These sky-high down payments are a big issue, because most American renters, and specifically Millennial renters, do not have that type of scratch.

Down payments have gone up way more than savings over the last three decades. (Source: Zillow / Federal Reserve)

Not even close, in fact. The typical 35-44 year old has about $5,000 in savings according to recent data from the Federal Reserve Survey of Consumer Finances. Meanwhile the typical <35 year old has less than $4,000 in savings. These savings amounts increased only marginally over the last three decades, while the down payment required to buy a home has spiked.

The expanding gap between the yellow and blue/orange lines on the graph signifies that Millennial-aged individuals are being priced out of the US Housing Market. Put simply – prices and the corresponding down payments are too high for most Millennials to afford.

To recap: the prime Millennial age segment is demanding a lower share of housing in recent decades while also losing ground on their financial ability to buy a home. Neither of those are good for Millennial Housing Demand in 2021/22. However, this last point drives the stake through the heart of the Millennial Housing Narrative.

Where are the Children?

Marriage and Children. These are the two most important drivers of sustainable, long-term housing demand. After a Millennial couple gets hitched, and when a baby is in the cards, the desire for owning a home switches from a want to a need.

Buying and owning a home provides the newlywed couple, or the expecting couple, with the space and security needed for growing a family. For them, homeownership confers real, intrinsic value beyond what an apartment or condo could ever provide. It’s for this reason that a Housing Market with a deluge of soon-to-be married, or newly married couples, will have robust housing demand potentially price growth for the foreseeable future.

However, there’s just one problem for the US Housing Market: Millennials aren’t as interested in getting married and having kids.

Fewer Households are having children and getting married. This is not good for the US Housing Market. (Source: US Census Bureau)

The graph above tracks two key data points: Households with their own Children (yellow line) and Married Households with their own Children (green line). Both lines paint a similarly bleak picture for fundamental demand in the US Housing Market.

After seeing an increase in the number of Households with Children from 1990 to 2007, there has been a steady decline since, with the 33.6 Million in 2021 registering below the level of the mid-1990s. Meanwhile, the number of Married Households with Children declined to 23.1 Million in 2021, the lowest level on record with the US Census Bureau.

At the same time, the share of adults who have never married spiked to 34% in 2021 according to US Census Bureau figures, a record high and far exceeding the levels of 25% in 1970. This suggests that Millennials and Gen Z are waiting longer and longer to settle down, start families, and have children (if they ever get around to it).

Ultimately this marriage and baby crash is bad news for the US Housing Market.

Fewer children, and fewer married couples with children, means way less urgency for individuals and couples to buy homes. Especially in a Bubble-Driven Market where most Millennials cannot afford the homes.

Millennials are Boycotting the Housing Market

The data is abundantly clear. Rather than bolstering the US Housing Market in 2021, Millennials are boycotting it. They’re 1) choosing not to form households, 2) don’t have the savings to afford today’s sky-high down payments, and 3) have record-low urgency coming from the family formation department. This means that Millennials are going to be predominantly renters, not homeowners.

Ultimately the Millennial Housing Market Narrative is just another in a long line of false “hype stories” to get more people, especially investors, to pile into a disastrously inflated Housing Bubble.

Speaking of those investors. Those are actually the ones supporting today’s market (not Millennials). Data from Redfin shows investors gobbling up a record-high 18% of all homes in the third quarter of 2021, triple the level of 20 years ago.

Was Tax Day more of a burden this year than years past? If you’re wondering whether there’s an escape from the inevitability of taxes let us give you the tools to analyze for yourself. Believe me, you’re not alone and not all states are created equal.

Home is where the heart is. Even in this volatile housing market you will always need a place to call home.

Has uncertainty and rising costs made home ownership unaffordable for many Americans? Let us provide some tools and analysis to help you find out for yourself.

The decision to buy or rent can be daunting and hopefully this methodology will help you in this monumental and stressful task. This article is meant to serve as a guide to assist in determining the true cost of home ownership for your situation.

Home Prices are up 20-30% across states like Florida and Texas in 2021. But there’s no growth in the number of people moving there. Is this a colossal bubble?

Florida’s Housing Market is BOOMING in 2021. But could the state be heading for another 50% crash in Home Prices? Certain data says that’s a possibility.

Surging Construction Costs in 2021 are being blamed for the Housing Market Mania being experienced in the US. Yet the data tells a very different story.

Where are the real estate markets that offer home buyers and investors the most value during the 2021 Housing Bubble? Reventure Consulting teaches you how to use data to find them!