The US Housing Market keeps hitting record highs each month.

The typical price of a home in America went up by an astounding 12% in early 2021 from the year prior, the highest increase since 2006 according to the Case-Shiller Home Price Index.

This run up in real estate prices is coming while there is a global economic depression. The US is still down 8 million jobs from its pre-pandemic high, while other countries are faring even worse. This has many asking: “Are we in a Housing Bubble?”

Media and real estate pundits, aware that this type of appreciation doesn’t make fundamental sense given today’s sour economic realities, have already come up a good excuse to justify current prices: Inflation! “Real estate might be pricey today, but it will be considered cheap in a year or two when inflation kicks in. Buy now!”

This is quite a seductive argument in May 2021. Price spikes in commodities such as lumber, copper, and oil have many concerned that a new era of hyperinflation could be around the corner. Others take a look at the generous Fiscal and Monetary policy of the last year and assume higher inflation is a given.

The problem with this argument? Real Estate is not the safe and steady inflation hedge it used to be. Instead, it has become a volatile asset class, with prices peaking well above inflation levels and crashing well below them. This shift started in the late 1990s three simultaneous triggers altered the perception of real estate from a boring store of value to a casino game.

Real Estate WAS a Good Hedge for Inflation

The perception of real estate as a good hedge against inflation was birthed in the 1970s. Back then, the US had extremely high rates of inflation, measuring above 6% per year for most of the decade, and even reaching a high of 14% in 1979. This rampant inflation eroded consumer purchasing power and was a massive issue for the economy, plunging the US into a four recessions from December 1969 to November 1982.

You can see those crazy high levels of inflation evidenced by the yellow line in the graph below, which tracks the year over year change in the Consumer Price Index (“CPI”) from 1955 to 1995.

Home Prices were a good hedge against Inflation in the 1970s. (Source: Fred / DQYDJ)

What’s also evident in this graph is that median home prices, the blue line, exhibit a tight historical relationship with inflation. When inflation was low in the 1950s and 1960s, home price growth was also low. But when inflation exploded in the 1970s, home prices followed suit.

Real estate was arguably the best performing asset class of the decade, far outpacing the stock market. The median price of a home in the US more than doubled from $24,000 in 1970 to $55,000 by 1980. Meanwhile the Dow Jones Index only increased by a meager 17% over the same time frame.

And so the perception of real estate a strong hedge against inflation was born.

Something Changed in 2000

For most of the 20th century real estate was a steady asset class. It appreciated at roughly the rate of inflation, which provided a great hedge for the inflationary period of the 1970s. But real estate was a very underwhelming performer in in almost all other time frames, measuring miniscule returns. In fact, over the entire 20th century – from 1900 to 2000 – inflation adjusted home prices only increased by 20% in total (0.25% per year)!

But something changed around 2000. Maybe it was a change in government policy and attitudes towards ownership. Or a new era of Federal Reserve intervention and low interest rates. Or a new cable TV channel that made real estate investor cool. Whatever the reason – perhaps a combination of all three – real estate prices started to detach from inflation.

The Inflation / Home Price Relationship Has Broken Down over the last 20 years (Source: Fred / DQYDJ)

First, starting in the late 90s and continuing through 2007, real estate prices appreciated at record, inflation-adjusted rates. Notice the large gap between the blue and yellow lines in the graph above around that time period. This continued outperformance of housing over inflation was a totally new phenomenon.

But then, of course, we all know what happened next. Home prices crashed from 2007 to 2012. Meanwhile, inflation dipped slightly in 2009, but soon rebounded back to the typical 2-3% per year level. Over the course of 15 years, real estate went from dramatically outperforming inflation to dramatically underperforming it. Something that had never occurred before in US history.

Then, sure enough, home prices began outpacing inflation again in 2013. And they’ve continued to do so since, accelerating all the way up a record inflation-adjusted increase in 2020/21 (largest gap between blue and yellow lines we’ve seen).

What’s going on here? Why has housing, which was once a stable asset that tracked inflation, become increasingly volatile? And what does that say about real estate as an inflation-hedge going forward?

HGTV and Investor Mania

Several big things took place at once in the mid-1990s:

Increased government support and subsidies for home ownership.

Active Federal Reserve which directly sought to “soothe” asset markets through low interest rates and quantitative easing.

The rise of HGTV.

The cocktail of these events was a perfect storm in stimulating frenzied interest in home ownership and investment. All of a sudden the house – which used to be viewed merely as a place to live – was now viewed as a path to riches. Let’s tackle these one by one.

Government Support and Subsidies: The US government sought to expand home ownership with the GSE Act in 1992, which required Fannie Mae and Freddie Mac to purchase a certain percentage of mortgages from low-income borrowers and low-income communities. The percentages outlined in 1992 were then significantly increased in 2000, particularly related to subprime borrowers, by then HUD Secretary Andrew Cuomo. The intention was to encourage banks to make more aggressive loans to economically fragile households, potentially contributing to the run up in home values and subsequent crash in the 2000s. And, perhaps more importantly, the GSE Act and subsequent amendments pushed the agenda of home ownership into the mainstream.

The Greenspan Put: Alan Greenspan was Chair of the Federal Reserve from 1987 to 2006. Greenspan’s Fed was a controversial one, particularly related to its loose monetary policy late in his tenure. Starting in December 2000, the Federal Reserve began a four-year course of lowering the federal funds rate, down from a high of 6.5% all the way to 1.0%, a historic reduction in a non-inflationary environment. Many speculate that Greenspan did this in response to the decline in stock market values that begin earlier in 2000, a signal to markets that the Federal Reserve was willing to lower interest rates for the sake of keeping asset prices high. While the stock market inevitably did crash over the next two years, many investors simply switched their focus and capital to the housing market, where mortgage rates remained low due to the Fed’s loose policy. We all know what happened shortly thereafter. Many believe that Greenspan’s loose policy from 2000 to 2004 set the precedent for the Federal Reserve to “bail out” asset markets with accommodative policy, thereby encouraging excessive risk-taking.

HGTV / House Flippers: The Home and Garden Television Network (“HGTV”) debuted on TVs across the nation in late 1994 to significant fanfare. It didn’t take long for the channel to gain significant traction and today it is the 4th most watched channel on cable TV. “House Hunters Renovation”, “Flip or Flop”, “Fixer Upper”, and “Property Brothers” brought the concepts of real estate investment and house flipping into the mainstream. Prior to the rise of HGTV it was mainly contractors and real estate agents who bought, renovated, and flipped homes, a fairly shallow market of local experts. But now, thanks to HGTV, nearly every household with some extra savings for a down payment is a potential flipper. The net result of this fanfare has been a massive increase in investor home purchases, increasing from approximately 6% in 2000 to 11% in 2018. The numbers in early 2021 are likely even higher. The increase in investor demand – particularly from amateurs – is likely increasing sales velocity and speculation in real estate markets across the country.

The Housing Bubble Trifecta: Momentum

These three factors have coalesced to form a Housing Bubble Trifecta – aggressive federal government support of home ownership, loose monetary policy intended to inflate asset prices, and a willing to investor pool spurred by HGTV. This Trifecta has transformed the US Housing Market from a slow and steady safe haven into a volatile casino.

The good times (2000-2006; 2013-2021) are assuredly very good. Prices go way up, blind optimism in the market says they can only continue to go up, and more and more home buyers and investors get sucked into the frenzy. Of course, that type of fever necessitates a boomerang effect, with the down periods (2007-12; 2022-???) hurting a lot more than they used to.

This Trifecta has also had other side effects. While the number of novice flippers is way up, so is the number of novice realtors. As of April 2021 the National Association of Realtors has 1.48 million registered members – above the previous peak set in 2006 before the last crash. Interestingly, there’s now more than 2x more registered realtors than there are active home listings in the US Housing Market. That’s a lot of people needing to hustle and convince others that buying is a good idea.

At the same time, the number of PropTech startups – technology companies whose business and associated revenue revolves around the housing market – has surged in recent years, increasing by nearly 8x from 2001 to 2021. These include large companies such as Zillow and Redfin, to go along with smaller ones such as Orchard and Pacaso.

All of these new flippers, realtors, and tech companies increase the momentum of the market. They all have a vested financial interest in perpetuating the housing market to higher and higher levels. As a result, not only do they drive prices higher and higher, they drive the narrative surrounding the housing market. So long as there are more and more stakeholders tied to housing market appreciation, mainstream narratives will choose to believe that home prices can only go up. You’re already starting to see that with articles like this, this, and this.

What Goes Up, Must Come Down?

As a result of the Housing Bubble Trifecta, its resulting momentum, and the continued detachment of home prices from inflation, I am skeptical that real estate will serve as the same type of inflation hedge now that it has in the past. When real estate was a steadier asset class, with less hype and momentum, it made more sense as an inflation hedge. But now that it has become a speculative asset, akin to the stock market, its correlation with inflation has decreased. Ultimately, one needs to ask themselves: do you like what the chart below is saying?

Home Prices are at their most expensive level ever relative to inflation. (Source: DQYDJ / Fred)

Home Prices are currently at their most expensive level ever relative to wages and other goods in the economy. As I’ve written about before on this blog, the US Housing Market looks to be in a bubbleby a host of metrics.

The widening gap between the blue and yellow lines in the graph above is unlikely to persist for much longer. Either home prices are coming down or inflation is going up. What’s going to happen next? In the end you need to make up your own mind, but I know what I’m betting on.

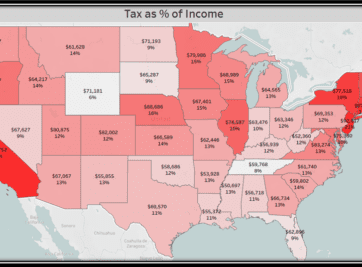

Was Tax Day more of a burden this year than years past? If you’re wondering whether there’s an escape from the inevitability of taxes let us give you the tools to analyze for yourself. Believe me, you’re not alone and not all states are created equal.

Home is where the heart is. Even in this volatile housing market you will always need a place to call home.

Has uncertainty and rising costs made home ownership unaffordable for many Americans? Let us provide some tools and analysis to help you find out for yourself.

The decision to buy or rent can be daunting and hopefully this methodology will help you in this monumental and stressful task. This article is meant to serve as a guide to assist in determining the true cost of home ownership for your situation.

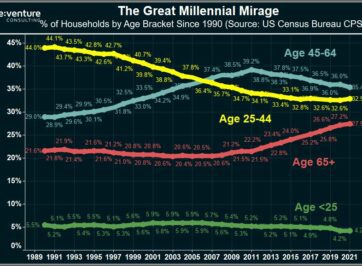

Millennials are supercharging the 2022 Housing Market, right? Wrong according to data from the US Census. In fact, Millennials are BOYCOTTING the Market.

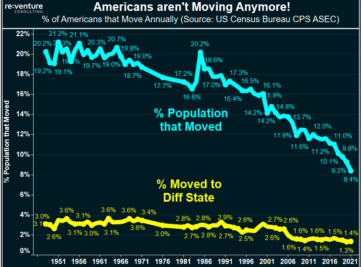

Home Prices are up 20-30% across states like Florida and Texas in 2021. But there’s no growth in the number of people moving there. Is this a colossal bubble?

Florida’s Housing Market is BOOMING in 2021. But could the state be heading for another 50% crash in Home Prices? Certain data says that’s a possibility.

Surging Construction Costs in 2021 are being blamed for the Housing Market Mania being experienced in the US. Yet the data tells a very different story.