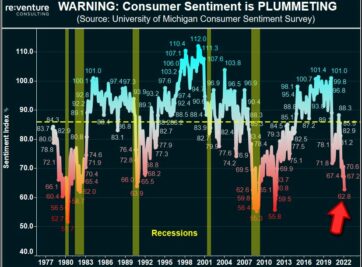

90% Chance: RECESSION in 2022?

Oil Prices are Surging. Consumer Sentiment is Crashing. The odds of a 2022 Recession have SKYROCKETED in recent months.

Luxury apartments (aka “Class A”) are deemed the safest investments in commercial real estate. Based on their perceived safety returns are low, with cap rates hovering from 4.0% to 5.0% for infill properties. Investors have been happy to accept these yields based on the downside protection they’ve been promised.

Yet several trends are emerging that call into question the perceived safety of luxury apartment investments. They include:

These risks are combining to put downward pressure on occupancy and rent growth. They’re also leading to an environment where free-rent incentives are becoming standard practice instead of just a lease-up tool.

Throw the COVID recession on top of these risk factors and the luxury apartment space, one thought to be largely insulated from downside risk, will experience significant haircuts to proforma cash flows and valuations over the next two years.

Since 2010 there have been over 15k new Class A apartment properties totaling over 3 million units delivered. There are another nearly 700k units under construction.

In the post-recession landscape of 2011 to 2013 new luxury deliveries conservatively ranged from 100k to 250k per year. But over the last several years new deliveries shot up to 375k-400k. The jury is out on what the final 2020 figure looks like due to COVID-related construction delays, however, it appears likely the figure will be close to 400k once again.

Meanwhile, aggregate occupancy rates for luxury apartments still remain in the mid-80% range (note this figure includes properties in lease-up). Stagnating occupancy rates in the face of new supply mean that the nominal amount of vacant units in the asset class is increasing at an alarming rate.

If we define luxury as anything built after 2011 (an incomplete assumption, but worthy of getting the point across), there are nearly 400k vacant luxury units in the United States today compared to 238k four years ago.

Thus, for new deliveries to lease-up while stabilized properties maintain occupancy, nearly double the number of units need to be absorbed today as compared to four years ago. And that’s not even considering the 700k units under construction.

If the demand for luxury apartments was growing at an accelerating rate these absorption hurdles wouldn’t be as concerning. However, there’s reason to believe the demand pool for this product type is flat or declining.

For one, the homeownership rate in the United States increased from 62.9% in 2016 to 65.3% in 2020. More homeowners equate to fewer households looking for rentals. Although its difficult to predict where the homeownership rate will trend in the coming years, accommodative fed policy looks poised to continue incentivizing home ownership.

On top of that, the rental rates for newly delivered luxury apartments are increasing at a much faster rate than incomes, decreasing the demand base for luxury properties.

Luxury properties delivered in 2011 had an average asking rent of $1,403 per month. As the decade went along each year brought new deliveries asking higher and higher rents. By 2019 the asking rent increased to $1,944, a nearly 40% increase and 4.1% CAGR over 2011 levels.

What is driving this rapid rent escalation? While wider amenity offerings and improved in-unit finishes likely account for some of the increase, general construction cost inflation is probably the predominant driver.

Turner Construction’s Cost Index ballooned by 42% from 2011 to 2019 (4.5% CAGR), an increase strikingly similar to the growth in new delivery rental rates. It’s likely that developers are passing off the construction cost inflation to tenants.

Yet incomes for renters haven’t followed suit. The incomes for skilled jobs (healthcare, business/financial, tech) only increased at an annual rate of 1.7% over the last decade. The result is that newly delivered luxury buildings, particularly those completed over the last three to four years, are becoming more unaffordable to renters.

Some tenants are happy to pay a higher share of income to rent for the amenities and lifestyle afforded by these properties. But others are beginning to get priced out, instead opting for lower-tier rentals or electing to buy given the low-interest-rate environment.

The 400k vacant luxury units, combined with the 700k under construction, will be even harder to absorb considering the rental rate escalation occurring. But there’s still yet another headwind that luxury properties face: the renters who do occupy these units are not very loyal.

The luxury apartment renter typically strikes a balance between having enough career progression to afford the high cost of rent but lacking enough personal life progression (marriage, children) to favor owning home. Thus, the window of opportunity for someone to prioritize living in a luxury apartment community is fairly small – maybe three to five years.

Rarely will upwardly mobile luxury apartment households stay at the same property in that window. Many will concession-hunt and bounce around from property to property in the same submarket. Others have jobs that will move them to different parts of the state or country.

The net effect of this limited leasing window and inclination to move is that luxury apartments maintain low retention rates. While a Class C property will typically renew 55-60% of its tenants each year, luxury properties fall in the 45-50% range.

Low tenant retention leads to increased vacancy and concession loss. It also results in higher turnover and marketing expenses. These operational issues eat away at yield and are exacerbated further when new supply hits the market.

The continuing onslaught of new supply, escalating rental rates, and a fickle tenant base combine to make luxury apartment investment riskier than the market anticipated. These trends were beginning to dampen investor returns over the last several years. Now, in the face of an economic recession, they will come front and center.

The accepted stabilized proforma of 5.0% economic loss and 3.0% rent growth will be replaced with 10-15% and 1.0%, respectively, over the next 12-18 months. As that occurs there will be heavy valuation haircuts – on the order of 20% – for refinancings and sales.

Class B and C properties, which don’t have as much supply competition and maintain a more loyal tenant demographic, will fare better. Properties in suburban areas, where there has been less supply expansion, will likely continue the trend of outperforming those in urban areas.

There are positive takeaways. Luxury apartments are still safer investments than office, retail, and hospitality. This will likely keep capital flowing into the asset space. Moreover, a decline in permitting is already underway, likely leading to a slowdown in supply expansion by 2022.

Enterprising investors should be able to capitalize on the current market dislocation and pick up distressed luxury properties at solid prices. The key over the next year will be to identify the markets and submarkets with the strongest growth prospects and heaviest supply constraints.

Oil Prices are Surging. Consumer Sentiment is Crashing. The odds of a 2022 Recession have SKYROCKETED in recent months.

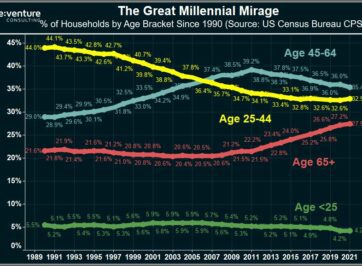

Millennials are supercharging the 2022 Housing Market, right? Wrong according to data from the US Census. In fact, Millennials are BOYCOTTING the Market.

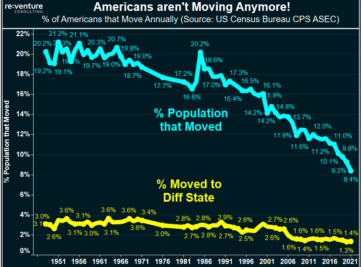

Home Prices are up 20-30% across states like Florida and Texas in 2021. But there’s no growth in the number of people moving there. Is this a colossal bubble?

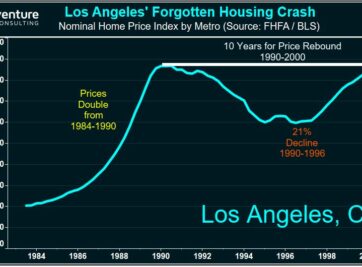

How bad will the 2021 Housing Crash be? Find out by looking back in history at the WORST Housing Crashes of all-time.

Florida’s Housing Market is BOOMING in 2021. But could the state be heading for another 50% crash in Home Prices? Certain data says that’s a possibility.

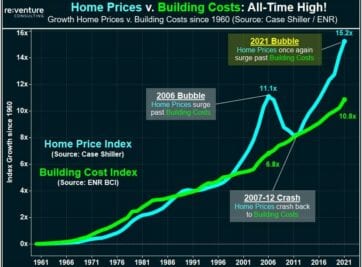

Surging Construction Costs in 2021 are being blamed for the Housing Market Mania being experienced in the US. Yet the data tells a very different story.

Where are the real estate markets that offer home buyers and investors the most value during the 2021 Housing Bubble? Reventure Consulting teaches you how to use data to find them!

Many pundits try to argue that the US is facing a housing shortage crisis. These people are wrong. In fact, the demographic data says the exact opposite – that there is a shortage in DEMAND for homes.

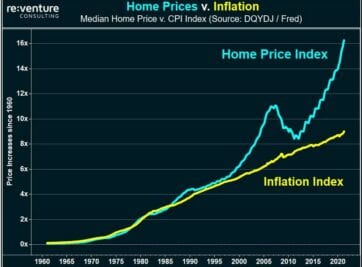

Prices in the US Housing Market are at record levels in 2021 relative to wages and inflation. Yet we’re in a deep economic recession. How could this be? Well, blame HGTV.

Sign up to hear insights from Reventure